We just published our 3Q20 reports where we looked at how the market performed during the three-month period from July to September.

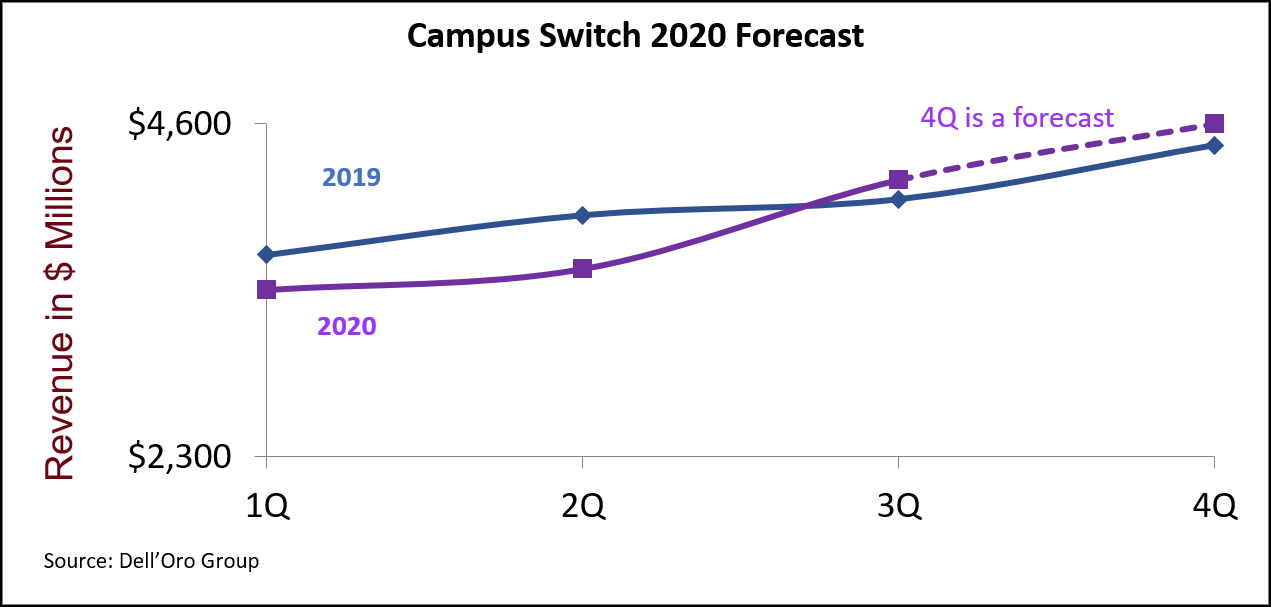

Surprisingly, the campus switch market performed well above our predictions in 3Q20. Revenue was up 3% Y/Y, compared to our prior forecast of a 12% decline, which would have been in line with prior recessions and in correlation with prior GDP forecasts.

The upside surprise was driven mainly by a stronger performance in North America as a result of strong government funding (CARES Act and E-Rate). Some of the manufacturers we interviewed expect government funding, mostly related to E-Rate, to flow into the next couple of quarters.

For 4Q20, we predict the market to grow at 3% Y/Y in 4Q20, in line with the 3Q20 performance.

We believe that the underlying growth drivers that helped the 3Q20 recovery will continue through the remainder of the year. We believe ongoing government funding, as well as improving macroeconomic conditions—namely in the U.S. and APAC—will encourage the large and even some mid-size enterprises in those regions to resume spending on infrastructure.

We would like to caution, however, that we may have underestimated the benefit from backlog fulfillment that may have artificially boosted the market performance in 3Q20. Some of the manufacturers we interviewed confirmed benefiting from backlog fulfillment during the third quarter as supply challenges improved. Those benefits from backlog fulfillment may not repeat themselves to serve as a tailwind in 4Q20. If that’s the case, our 4Q20 forecast may be too high.

For the full year of 2020, we currently predict the market to decline only 2%, as the anticipated recovery in 2H2020 will offset some of the weakness in the first half of the year (1H2020 was down 8% Y/Y).

Campus switch revenue forecast to return to growth in 2021

Looking at 2021, we predict the positive momentum to continue and drive 2% growth in the market. This projected growth will be propelled by improvement in macro-economic conditions as recent GDP reports indicate that economists at world-leading banks are forecasting positive GDP growth in 2021, compared to negative growth in 2020. Additionally, the availability of a vaccine will help abate the uncertainty in the market and boost business confidence.

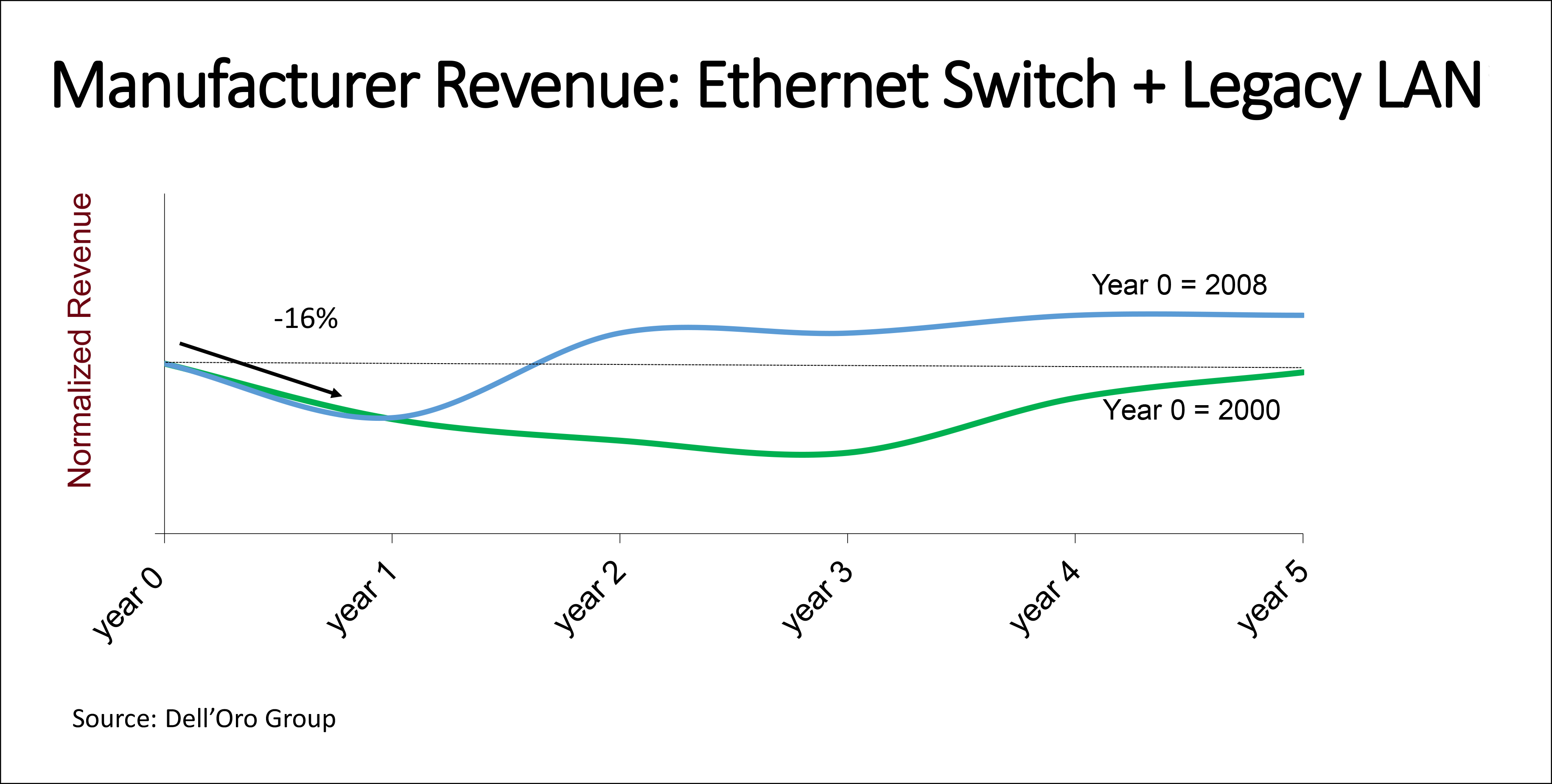

This pandemic-induced recession looking better than the two prior ones

The question now is how this projected performance in the market compares with the performance during the two prior recessions (in 2000 and 2008). In the 2000 recession, sales of enterprise switches declined in the mid-teens in the first year of the recession and it took the market three years before returning to growth. In the 2008 recession, the market declined in the mid-teens in 2009 as well, but returned to growth in the following year, thanks to deep government stimulus. We believe a few major tailwinds would help the market perform better during this pandemic-induced recession.

First, government spending and stimulus helped not only the government sector but also the lower-education vertical and even manufacturing as governments in some regions of the world, such as Asia Pacific, provided incentives to manufacturers to modernize their processes.

Second, China, which recovered relatively fast and has been providing some uplift to the market since 2Q20, is now a significant portion of the total sales. (China was less than 10% of the market in 2008 and prior vs. about 20% in 2019).

Third and more importantly, this pandemic has actually amplified the importance of the network and is accelerating the digital transformation and network upgrade cycles. Our interviews with end-users as well as system integrators revealed that some of the digital transformation projects have been pulled in by about one to two years. This accelerated pace of digital transformation is offsetting some of the impact from work from home and cannibalization from WLAN, which we are planning to discuss in more details in our upcoming five-year forecast report.

Despite our optimism, a lot of uncertainty remains in the market

Despite our optimistic outlook, we wouldn’t be surprised if the market continues to show some volatility next year. We believe the level of uncertainty in the market remains relatively high due to elevated levels of unemployment rate and bankruptcy. Additionally, our interviews as well as commercial real estate reports are showing decreased demand and high level of excess capacity which may potentially impact demand for network equipment. We question whether the true level of private demand is currently camouflaged by massive government funding.

Finally, it bears mentioning that at the time of this writing, the rate of infections is accelerating, prompting many countries to slow business reopening, while invoking curfews and lockdowns. This may potentially suppress market growth but we believe that the impact will not be as significant as what the market has experienced with the first wave of infections and lockdowns. We believe that many vendors, as well as their customers, have figured out ways of doing business during the unusual circumstances in these unprecedented times.

All that said, although we believe the worst of the pandemic is behind us, we are all watching how fast and smooth the distribution of the vaccine will be. Until then, and until the vast majority of the population is vaccinated, a lot remains uncertain about the outcome of this pandemic.