Originally, I anticipated that the Microwave Transmission market would enter a multi-year growth phase beginning in 2020 driven by the rollout of 5G. Instead, however, the market is on pace to decline 5 percent in the year due to precautions put in place to reduce the spread of COVID-19, slowing down the start of 5G in some countries and making it increasingly difficult to deliver and install microwave equipment in many others. Then in 3Q20, when many countries lifted their lockdowns or eased travel restrictions, the demand for Microwave Transmission equipment grew 7 percent year-over-year, recovering some of the lost market revenue in 1H20. We think this positive momentum will continue through the remainder of this year and the next. So, while the start of 2020 was painful and the middle of 2020 difficult, the end of 2020 brings some hope for a better 2021.

Of course, there will be a number of head winds in 2021—the biggest ones being additional lockdowns to control the spread of COVID-19 and the slow economic recovery. Both of these will negatively influence the revenue and confidence of mobile operators in spending capital on equipment.

That all said, we believe that COVID-19 has taught the world the critical importance of network connectivity. Whether it is fixed broadband or mobile broadband, there will be a need for “more”—more connections and more bandwidth. Therefore, while COVID-19 may have caused delays in starting new 5G roll outs in 2020, we find it difficult to believe there will be additional delays in 2021 since 5G is a crucial technology for the future.

Hence, we predict that the Microwave Transmission market will return to growth in 2021 (one year later than we had originally predicted). We believe 5G and preparation for 5G mobile radio installations will create a growing demand for Microwave equipment in 2021 and project the market to grow at a low single digit percentage rate. Furthermore, we think this is just the beginning of a multi-year growth cycle.

Since 5G will require more backhaul capacity, we expect the demand for E-band microwave systems (capable of up to 20 Gbps transmission) will accelerate, increasing more than 30 percent next year. While sales of E-band has been escalating for many years, largely driven by its use in Eastern European countries, we think that next year the level of interest and number of deployments will geographically widen across many other regions of the world.

Also, we think multiband systems and links combining E-band with at least one carrier frequency below 30 GHz will grow in importance. Demand for multiband systems using a mix of millimeter wave and lower microwave frequencies has already started in 2020, but we think usage will widen in 2021 along with 5G backhaul deployments. Not only will this solution provide more capacity per link, but it will also increase the link resiliency and performance with the same outdoor footprint (keeping tower lease costs unchanged). Therefore, we cannot help but think that the adoption of multiband links will be more mainstream than niche in the coming year.

Although we have a positive outlook for 2021, we do think the market will be more volatile. This is not to say that the demand for Microwave Transmission equipment will swing up and down quarter-to-quarter (which it might), but rather that the level of uncertainty in 2021 is still very high. And that while we are hopeful the worst of the pandemic is behind us and the COVID-19 vaccine will be widely distributed next year, it is still difficult for us to discern what will happen because when it comes to this pandemic (the first in my history of doing market research) we simply do not know what we do not know.

[wp_tech_share]

AI and Network Virtualization Drive Overall Market Changes

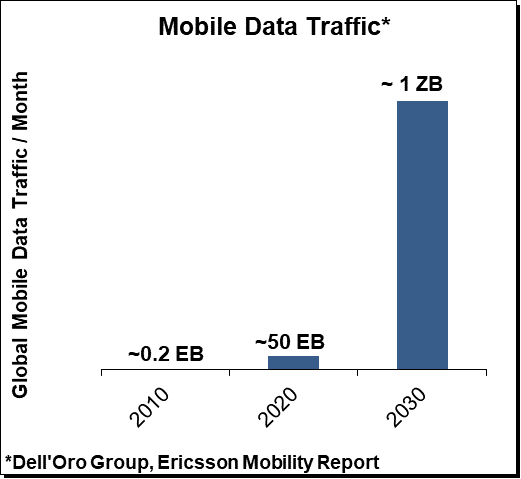

The quickening pace of technological innovation across a growing number of industries will drive continued growth in the semiconductor industry. In the communications and consumer electronics verticals, the global deployment of 5G mobile and fiber-based broadband networks along with the phones and other devices used to access those networks and services, will be significant drivers of new semiconductor designs. Additionally, the proliferation of AI (Artificial Intelligence) and machine learning throughout service provider, cloud hyperscaler, enterprise, and industrial networks, will also drive demand for chips with embedded processing capabilities.

From a regional perspective, the Asia-Pacific region will continue to provide the largest source of revenue for the overall semiconductor industry, as China will remain the world’s largest importer and purchaser of components. China is estimated to purchase roughly 40% of worldwide semiconductor shipments, with an estimated 80% of semiconductors used in communications and consumer electronics product designs estimated to be imported from abroad. However, the domestic Chinese semiconductor manufacturing industry is estimated to be capable of meeting at most 30% of total demand.

This large discrepancy has resulted in a massive trade and technology deficit, which the Chinese Government is attempting to balance through a combination of subsidization, private equity, and the lowering of barriers to entry for foreign participants. The primary goal of these efforts is to advance the overall semiconductor industry to increase self-reliance and reduce the uncertainty that has arisen due to ongoing trade tensions with the US and other Western countries.

In 2014, China’s State Council published the “National Integrated Circuit Industry Development Guidelines,” which proposed to set up a special industry investment fund to back domestic semiconductor startups, particularly around 14nm finFETs, memory, and packaging. The “Big Fund,” as it is called, has gone through two rounds of funding, most recently raising around $29 billion in 2019.

The coordinated efforts have resulted in some notable advances, including SMIC’s (Semiconductor Manufacturing International Corporation) capability of shipping 14nm finFETs with 7nm in R&D. This is an advance over just one year ago, when SMIC’s most advanced process was a 28nm planar technology. Additionally, China will spin up its first 28nm lithography machine in either 2021 or 2022, which will help Chinese companies manufacture advanced 28nm chips, possibly within 1-2 years. That would be a significant step forward for the domestic industry and provide a foundation for more domestic foundries to begin more advanced design and manufacturing for 14nm and 7nm-based processors.

Ramping up 28nm chip production is an important milestone for the Chinese industry, as there will remain a large market for trailing-edge chips as AI features and functionality are embedded in more consumer electronics, automobiles, robots, smart electric meters, smart traffic lights, etc. The AI chips used in these applications will require more leading-edge chipset design, as opposed to leading-edge fabrication. Thus, the short-term goal of achieving scale at 28nm is a very meaningful step in the long process of developing a more complete, domestic IC ecosystem.

SMIC is also on the verge of building out a $7.6 billion plant in Beijing that will produce 12-inch wafers with the intention of fabricating 28nm chips. This factory, along with the expected buildout of other plants, could help to solve one of the Chinese industry’s biggest hurdles to the global competition: production capacity.

Additionally, SMIC and other manufacturers are also in the process of adding both foreign and domestic technical talent with the necessary years of experience to design and manufacture high-quality chips with consistent performance at price points that are competitive. These efforts will ultimately benefit the overall industry and supply chain, though the results will take time. Currently, SMIC’s top wafer production is at 14nm, while others are at 7nm and already pursuing 5nm and 3nm processes. Though improving and evolving its production knowledge and facilities are important goals, the company must still balance being the primary supplier of chips that don’t necessarily require the latest nodes. That balance is just as important to the overall growth of the semiconductor industry in China as is the ultimate evolution to 14nm and 7nm production capabilities.

When it comes to AI chips, specifically—including GPUs (Graphics Processing Units) and FPGAs (Field Programmable Gate Arrays)—Chinese companies are still expanding their knowledge and capabilities to compete effectively in what is expected to be a massive market over the next decade. These are the chips that are the most heavily in-demand for communications networks, especially as these networks are transformed and processing capabilities are distributed to the edge of the network and away from centralized data centers and central offices. The result will be smaller platforms supporting and processing the data traffic coming from billions of connected devices.

Currently, Chinese FPGA makers and network equipment providers license cores from Western companies, such as Intel and ARM. These companies also rely on EDA (Electronic Design Automation) software from Western companies, such as Cadence. Despite recent trade tensions, Chinese firms need these partnerships to continue to deliver their products to the market. These Western vendors also depend heavily on the China market for their revenues.

Although China is investing heavily in building out its semiconductor capacity, the innovation capacity advantage enjoyed by US and Western countries means that Chinese companies will continue to need access to US and Western technology for core components, software, design, and systems integration. For Western companies, this means that new market opportunities have opened up for them, provided that concerns around intellectual property, forced technology transfer, and cybersecurity are understood and that these Western firms continue to remain ahead on the innovation curve.

The opportunities for cooperation are there but will require effort to ensure both sides have their concerns around competition and information security are acknowledged and addressed. There is no question that Chinese firms will continue to move down a path towards more self-sufficiency when it comes to the design and manufacturing of leading-edge semiconductors. The investments that have already been made and will continue to be made by both existing semiconductor companies, as well as government and private investment, will ultimately result in a more self-sufficient ecosystem in China. It will take a combination of industry maturity, trial, and error, along with a focus on mass production and scale. Given the size of the investments being made coupled with geopolitical uncertainty that is accelerating the drive towards self-sufficiency, the Chinese semiconductor ecosystem could potentially close the gap faster than expected.

[wp_tech_share]

Open and Virtual RAN continues to gain momentum, bolstered by Ericsson now formalizing its support with its Cloud-RAN announcement. The uptake remains mixed. In this blog we will discuss three key takeaways for the 3Q20 quarter including:

1) The primary objective of Open RAN is to address market concentration and vendor lock-in;

2) Open RAN revenues are trending ahead of schedule;

3) Not all Open RAN is disruptive.

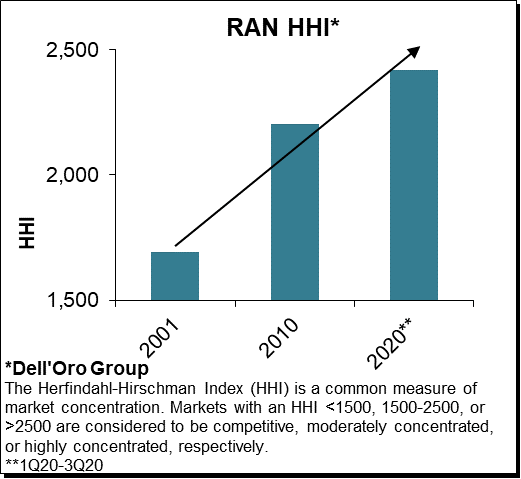

First, when it comes to the broader movement behind Open RAN, the leading drivers have not changed since we published the Open RAN Forecast this August. Addressing vendor lock-in and market concentration remain the leading drivers behind the Open RAN movement. Initial readings suggest that the overall RAN market concentration levels as measured by the Herfindahl-Hirschman Index (HHI) increased around 10% between 2010 and 1Q20-3Q20, underpinning projections that these trends will not reverse anytime soon with the current RAN model.

Preliminary estimates suggest Open RAN revenues – including radio, baseband, and software – are coming in at a slightly faster pace than initially expected, reflecting positive developments in the Asia Pacific region. We have adjusted the 2020 outlook upward from ~$0.2 B to ~$0.3 B.

Even though we are in the middle of updating the long-term projections, at this point we just want to clarify that the stronger than expected short-term acceleration does not necessarily translate to faster or slower brownfield adoption beyond 2020.

The results are mixed. While Dish is running into delays in the US market, Rakuten is moving forward at a rapid pace in Japan deploying a variety of both sub 6 GHz and mmWave RAN systems. In addition, some of the Japanese suppliers are reporting that the lion share of their radio shipments are already O-RAN compatible.

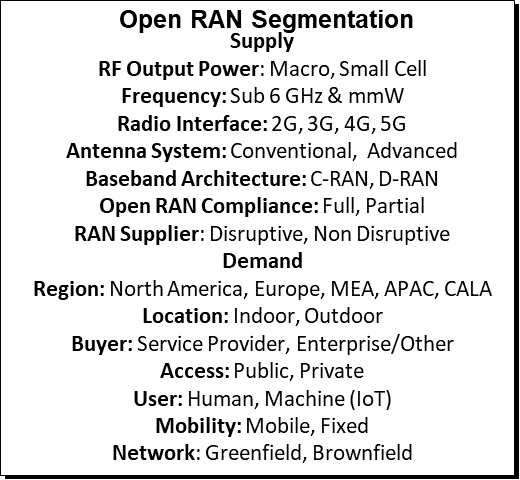

The last point we want to make is that not all Open RAN is the same. There is no shortage of ways to segment the Open RAN market – at a highly simplified level, we envision there at least 14 ways to think of the Open RAN opportunity. And while revenue remains a fundamental metric to determine the overall market adoption, it will be particularly interesting to pay attention to the RAN supplier segmentation. This will be important to assess if Open RAN is also disruptive. Because at the end of the day, Open RAN will likely not be considered a complete success story even if Open RAN comprises 100% of the total RAN market but the HHI is still hovering around 2500.

So on the one hand, we estimate total Open RAN revenues are tracking ahead of schedule. On the other hand, the lion share of any “security” related RAN swaps are still going to the traditional RAN players, suggesting the technology for basic radio systems remains on track but the smaller players also need to ramp up investments rapidly to get ready for prime time and secure larger brownfield wins.

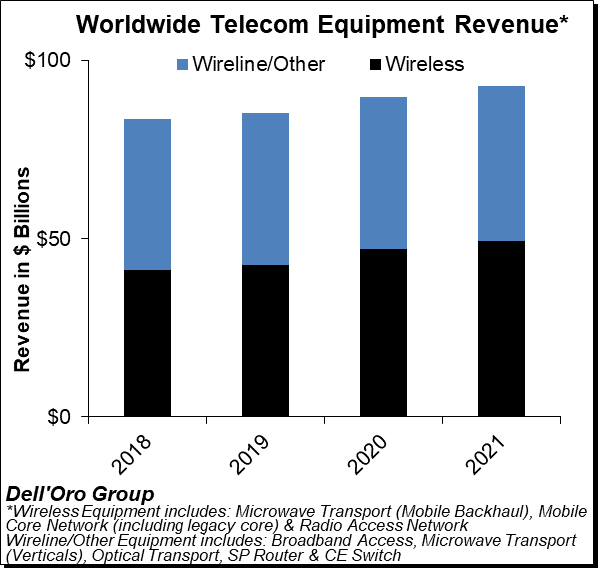

We just wrapped up the 3Q20 reporting period for all the Telecommunications Infrastructure programs covered at Dell’Oro Group. Preliminary estimates suggest the overall telecom equipment market – Broadband Access, Microwave & Optical Transport, Mobile Core & Radio Access Network, SP Router & Carrier Ethernet Switch (CES) – advanced 9% Year-Over-Year (Y/Y) during 3Q20 and 5% Y/Y for the 1Q20-3Q20 period.

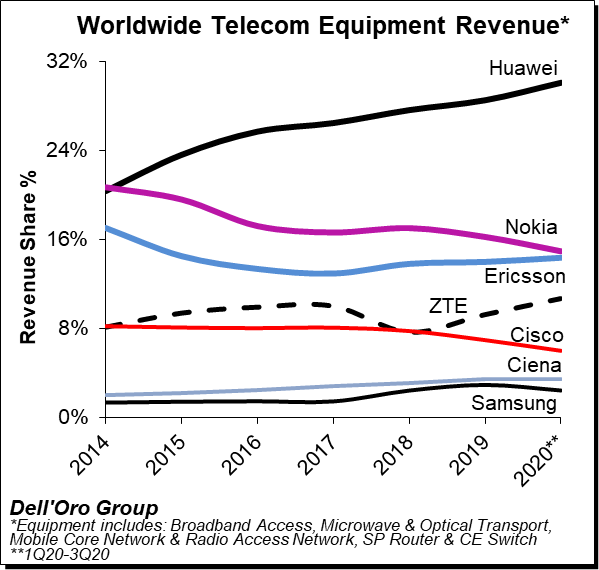

The analysis contained in these reports suggests revenue rankings remained stable between 2019 and 1Q20-3Q20, with Huawei, Nokia, Ericsson, ZTE, Cisco, Ciena, and Samsung ranked as the top seven suppliers, accounting for more than 80% of the total market. At the same time, revenue shares continued to be impacted by the state of the 5G rollouts in highly concentrated markets.

We estimate the following revenue shares for 2019 and the 1Q20-3Q20 period for the top seven suppliers:

Top 7 Suppliers

Year 2019

1Q20 to 3Q20

Huawei

28%

30%

Nokia

16%

15%

Ericsson

14%

14%

ZTE

9%

11%

Cisco

7%

6%

Ciena

3%

3%

Samsung

3%

2%

Additional key takeaways from the 3Q20 reporting period include:

Following the 4% Y/Y decline during 1Q20, the positive trends that characterized the second quarter extended into the third quarter, underpinned by strong growth in Optical Transport and multiple wireless segments including 5G RAN, 5G Core, and Microwave Mobile Backhaul. Technology segments that were impacted more materially by COVID-19 and the lockdowns during 1Q20 continued to stabilize in the quarter.

Preliminary estimates indicate increasing Mobile Infrastructure and Optical Transport revenues offset declining investments in Microwave Transport and SP Routers & CES for the 1Q20-3Q20 period.

The overall telecom equipment market continued to appear disconnected from the underlying economy. While the on-going transition from 4G to 5G is helping to offset reduced capex in slower-to-adopt mobile broadband markets, we also attribute the disconnect to the growing importance of connectivity and the nature of this recession being different than in other downturns improving the visibility for the operators.

With investments in China outpacing the overall market, we estimate Huawei and ZTE collectively gained about 3 percentage points of revenue share between 2019 and 1Q20-3Q20, together comprising more than 40% of the global telecom equipment market.

The Dell’Oro analyst team has not made any material changes to the overall outlook and projects the total telecom equipment market to advance 5% to 6% in 2020 and 3% to 4% in 2021. Total telecom equipment revenues are projected to approach $90 B to $95 B in 2021.

Dell’Oro Group telecommunication infrastructure research programs consist of the following: Broadband Access, Microwave Transmission & Mobile Backhaul, Mobile Core Networks, Mobile Radio Access Network, Optical Transport, and Service Provider (SP) Router & Carrier Ethernet Switch.

[wp_tech_share]

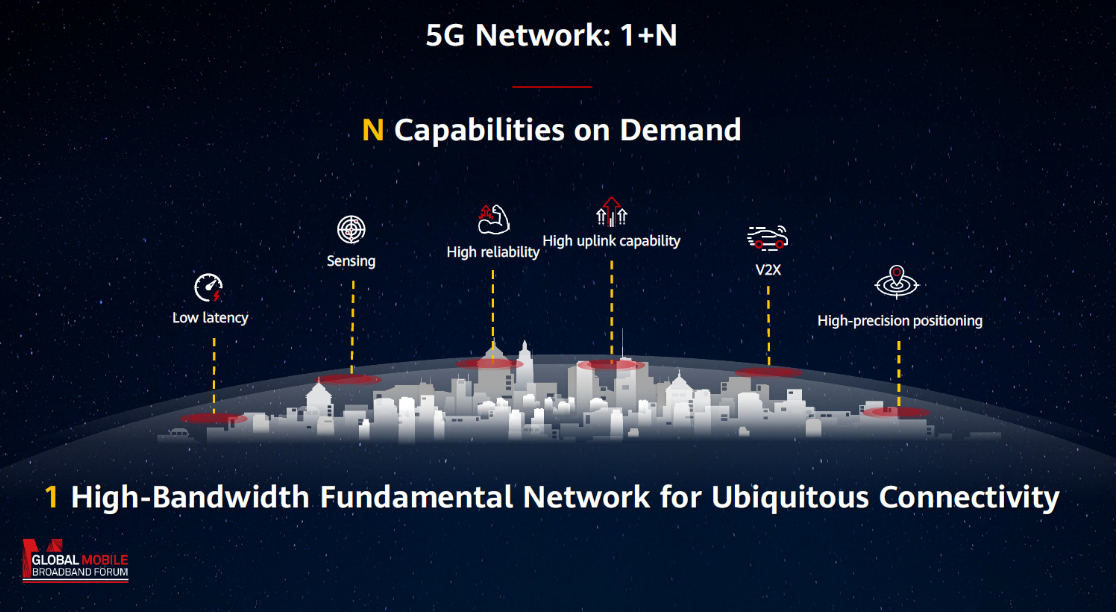

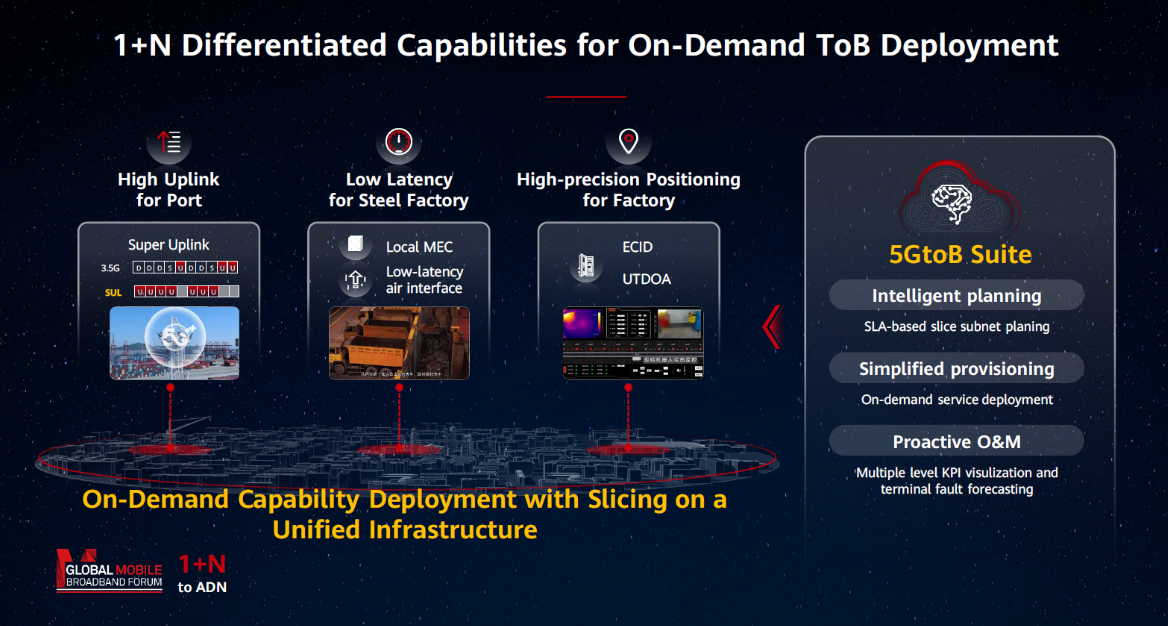

Huawei recently held its annual MBBF Forum. Even though we were not able to attend in person, it was an interesting event. Below we will add some color to five radio access network (RAN) related takeaways including 1) 5G=1+N; 2) Massive MIMO is a massive success; 3) There is more room left in the sub 6 GHz tank; 4) Site simplification will play an increasingly important role; 5) The outlook for vertical 5G activity is improving.

5G = 1+N (One foundational network plus N capabilities on demand)

If there is one thing we can all agree on after these first two years of commercial 5G deployments, it is that 5G means different things to different people.

While there is little disagreement that 5G now initially is just another G, providing operators with a compelling technology and business case to expand their respective mobile broadband networks to address todays use cases, the interpretation about the 5G opportunity tends to become more interesting as we look beyond the smartphone MBB use case. Because even if the narrative has morphed somewhat and the lion share of the capex in this initial wave is addressing what we know today, the long term vision still holds, namely that 5G has the potential to expand the role of connectivity beyond the MBB usage scenario and pave the way for new applications and use cases and expand the wireless based economy.

In order to address both the known and unknown opportunities with extremely diversified service requirements, Huawei is recommending operators build one foundational wide-area mobile broadband network with ubiquitous connectivity. The vision here is resting on the assumption that this foundational network combined with flexible on demand capabilities leveraging various spectrum bands (such as those designed for FDD or Super Uplink) to address diversified 5G service requirements for various people, things, and industries will ultimately enable the operators to provide optimized solutions from a technology and business case perspective for the various 5G opportunities.

Huawei MBBF 2020

Huawei MBBF 2020

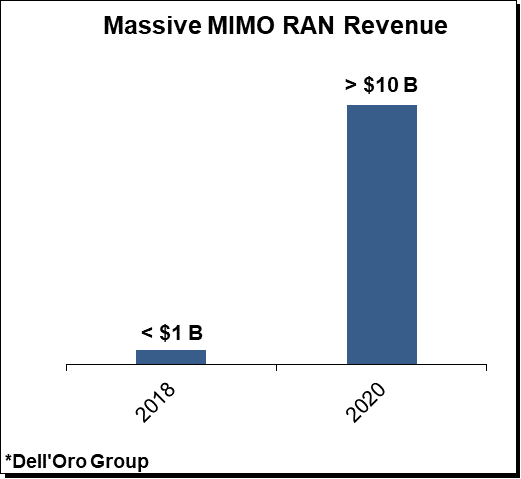

TDD Massive MIMO is a mainstream technology

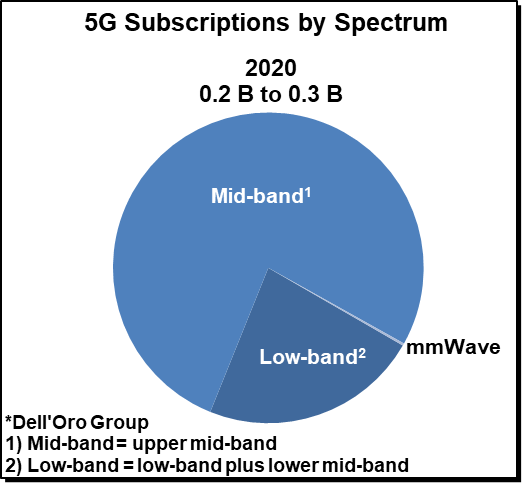

For a technology that was initially viewed as being mostly a fit for hotspot scenarios, Massive MIMO has come a long way, accelerating at a much broader and faster pace than initially expected. Preliminary estimates suggest Massive MIMO RAN investments remain on track to surpass $10 B for the full-year 2020, up nearly 20-fold in just two years. Cumulative Massive MIMO transceiver shipments are projected to approach 0.1 B to 0.2 B in 2020.

Not surprisingly, Massive MIMO based technologies are powering the vast majority of the 100+ commercial 5G networks. And more than 75% of the projected 0.2 B+ 5G subscriptions by year-end 2020 will likely utilize the upper mid-band.

While Massive MIMO has surprised on the upside when it comes to form factor, weight, performance, cost, and price, one of the key takeaways from the event was that this technology has more room to advance and will continue to play an extremely important role going forward.

Sub 6 GHz enhancements

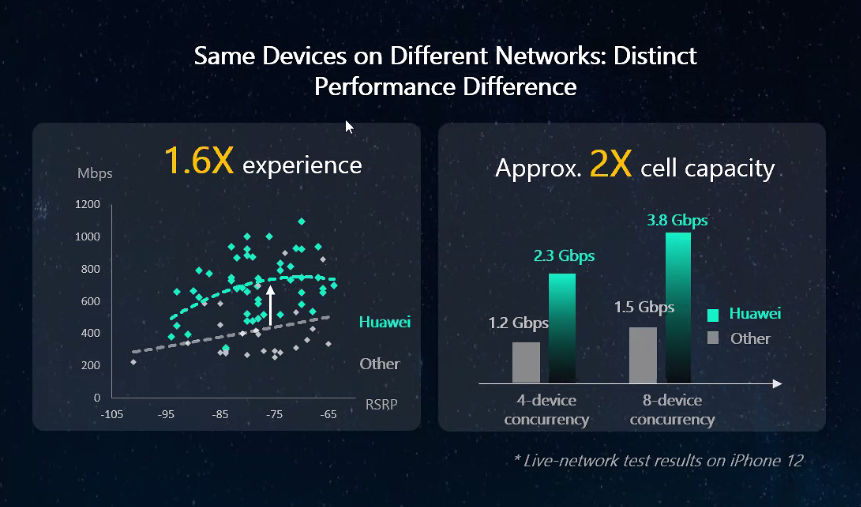

During the event, Huawei discussed the prospects of another potential 2x of cell capacity using its Adaptive High Resolution (AHR) algorithm to enable a premium experience in locations with high user density and interference.

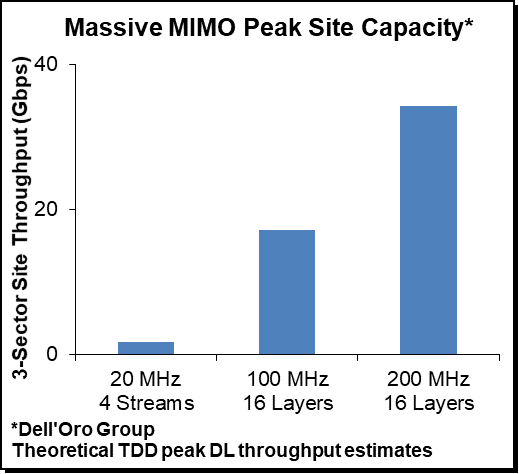

There is indeed something to be excited about. In this scenario, theoretical 3-sector peak capacity would approach 17.1 Gbps if used in conjunction with the AHR (100 MHz of BW, 8 users). This is consistent with Ericsson and T-Mobile’s recent 16-layer MU-MIMO demo with peak cell throughputs of 5.6 Gbps.

More importantly, Huawei also shared data from real deployments, showing that these types of algorithms can improve the performance outside the lab in non-ideal conditions producing around 3.8 Gbps of cell capacity in 100 MHz of bandwidth.

Huawei MBBF 2020

Huawei also signaled some optimism about the FDD Massive MIMO opportunity, announcing the FDD-based 32T32R system, primarily targeting operators with limited upper mid-band spectrum. As a reminder, FDD-based Massive MIMO systems are not new and this concept has been around for some time. However, FDD-based Massive MIMO technologies have not gained the same mass-market acceptance as TDD-based solutions. In addition to the relative efficiency gap between FDD and TDD as a result of leveraging channel reciprocity in TDD systems, FDD-based solutions typically also operate in a lower spectrum band, increasing the physical size of the antennas.

Measuring 0.5 meters in width and weighing around 50 kg, it remains somewhat unclear at this juncture how operators will prioritize FDD-based Massive MIMO in the broader long-term capacity roadmap. Even though preliminary Huawei tests suggest 32T32R can deliver 3x to 4x of capacity growth relative to 4T4R, we expect that FDD Massive MIMO adoption will remain limited for some time and likely be a stronger candidate for mass-market acceptance once operators exhaust the upper mid-band spectrum. At that point, operators can assess what the best tool in the toolkit might be to deliver the next most economical and sizeable capacity boost – FDD Massive MIMO, 6425-7025 MHz, or mmWave.

Site simplification

One of the reasons this shift from passive 4G to active antenna based 5G has accelerated at a much faster pace than initially expected is the fact that operators can for the most part leverage their existing macro grid, which has been a major benefit both from a time-to-market and TCO perspective as it reduces the need to add more outdoor sites to realize 5G NR coverage that is equivalent to the outdoor sub 3 GHz LTE coverage. This model of adding new technologies to the existing sites at a faster pace than legacy technologies are sunset will naturally complicate the situation as the sites are becoming increasingly crowded. Although suppliers have invested heavily to address some of the shortcomings at the site with more power-efficient systems and smaller form factors to manage the challenges with adding both Massive MIMO and non-Massive MIMO configured systems, there is more work to be done to support the various frequency and passive/active antenna systems.

During the MBBF event, Huawei announced various RAN enhancements as part of its continuous journey to simplify site deployments including the Blade AAU Pro, which combines a 64T64R 200 MHz Massive MIMO antenna with passive sub 3 GHz band support. As a reminder, Ericsson has its Hybrid AIR antenna system and Nokia and CommScope recently announced they are working on a new hybrid passive/active antenna solution addressing similar site challenges. Huawei is claiming this is the first 64T64R and full sub 3 GHz hybrid unit.

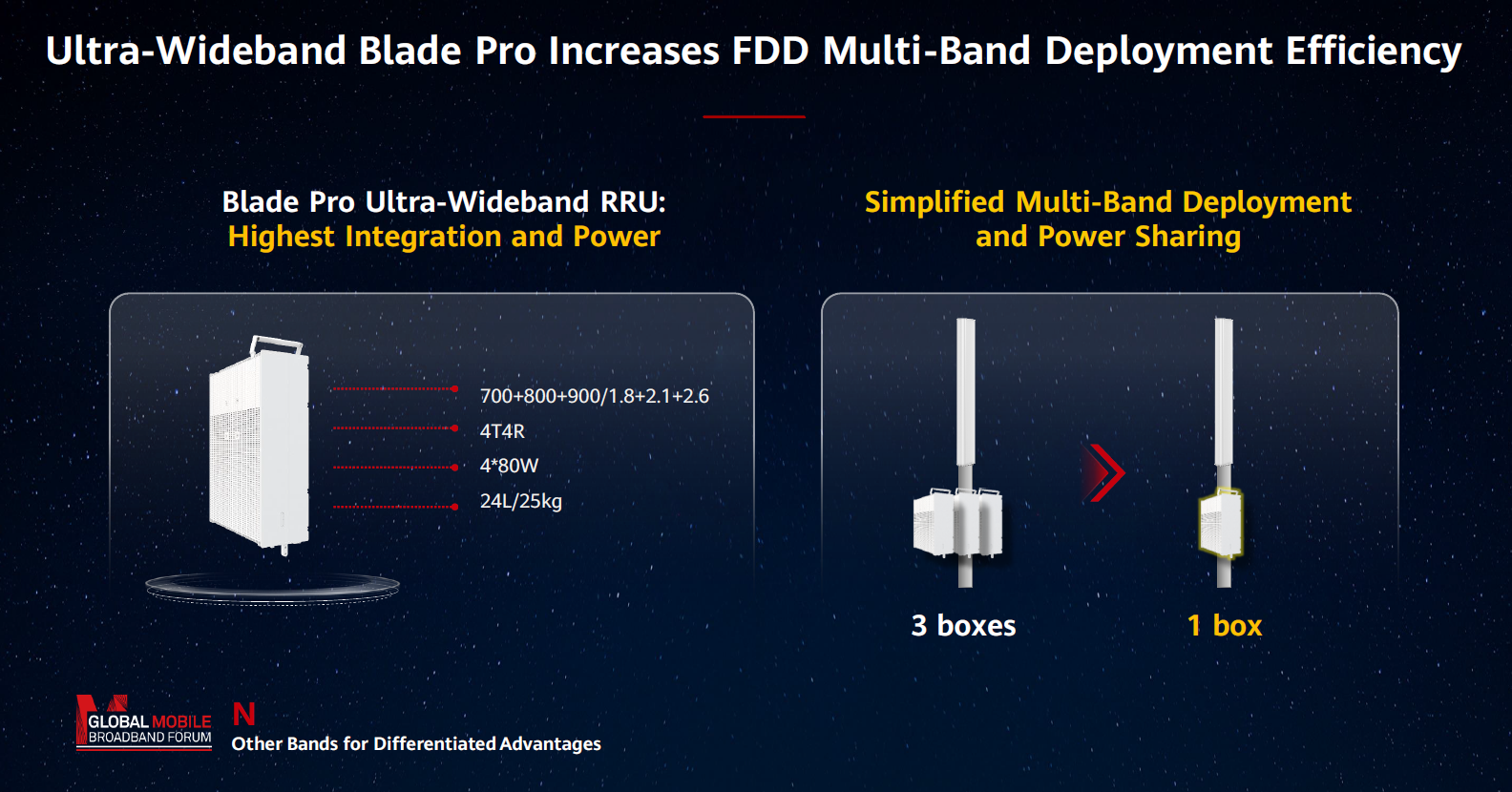

Also, Huawei released its highly integrated Blade Pro portfolio for FDD applications. This portfolio includes the Blade Pro Ultra-Wideband RRU, which reduces the number of required devices at the cell site by integrating three low-band or three intermediate FDD bands into one box, providing operators with more tools to simplify and manage increased site complexity.

Huawei MBBF 2020

In addition to the increased focus on form factor, power consumption, and radio integration, this on-going shift towards multi-technology sites addressing legacy technologies and all the various 5G solutions targeting a wider scope of use cases spanning across potentially multiple industries will also complicate the overall site simplification objective from an operations & maintenance (O&M) perspective. In order for the operators to maintain the performance for 2G-5G consumer networks and simultaneously target capabilities for vertical opportunities while balancing the user experience and optimizing the use of the all the resources to ensure the right KPIs are delivered without breaking the energy or opex budgets, increasing the reliance on more intelligent solutions will be paramount. During the event, Huawei reiterated the importance of introducing more intelligence to simplify the networks and manage the increased complexity without growing opex. AI-assisted autonomous driving of networks will play an increasingly important role to address the challenges O&M poses in the 5G era.

The outlook for vertical 5G is improving

5G eMBB (and FWA) is driving the lion share of the current 5G RAN capex (>99%), still, one of the more exciting takeaways from this event was the progress beyond the eMBB/FWA use cases. At a high level, it is still very early days for private wireless, which is currently dominated by LTE. The private 5G market is even more nascent but with standards ready, 5G and private spectrum becoming available, an ecosystem that is accelerating, and signs of activity picking up pace as new use cases are emerging, there is some optimism that private wireless and 5G NR 2B capex can become more meaningful in the next couple of years.

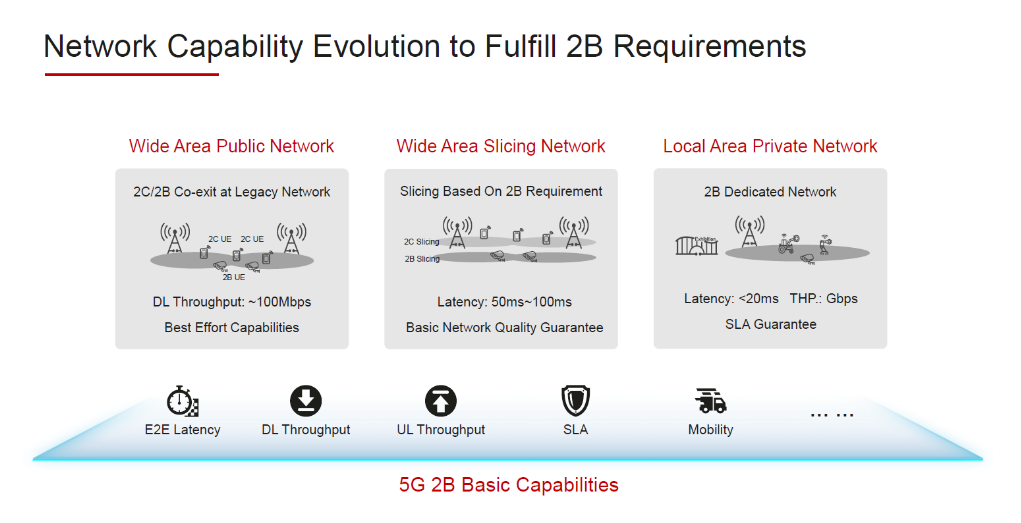

Huawei’s 2B segmentation is consistent with how the broader industry is now characterizing this market opportunity, consisting of three high-level tiers including the Wide Area Public Network, Wide Area Slicing Network, and Local Area Private Network. Some suppliers are also considering splitting the Wide Area segment into two tiers to capture the various coverage ranges.

Huawei MBBF 2020

What makes the private and 2B markets so exciting is that the opportunities are so vast for both the operators and the suppliers. At the same time, private wireless is different than the traditional public wireless market not only from a technology and standards perspective but also from an ecosystem, go-to-market, and deployment perspective.

Revenues are small relative to overall 5G investments but activity is on the rise. Huawei is engaged in thousands of private 5G projects across China focusing on smart factory, smart port, smart mining, smart utilities, and smart healthcare — consistent with its four-dimensional strategy to move from demo to deployment assessing the opportunity and readiness from a business, technology, standard, and ecosystem perspective. Judging by the proof of concept data shared at this event and progress communicated by other RAN suppliers, the smart factory appears to be emerging as a common theme.

As we have discussed in the 5-year forecasts, it will take time for these non-traditional opportunities to offset declining macro coverage capex post the peak MBB rollout phase. Nonetheless, the progress is promising, bolstering the thesis that the aggregate upside of these smaller opportunities could provide some cushion in the outer part of the forecast period.

The event was also a good reminder that the smaller Open RAN suppliers need to ramp investments to ensure they can deliver simplified and energy-efficient passive/active/hybrid solutions in a competitive form factor that maximizes the use of the sub 6 GHz spectrum.